Most employees look forward to a new financial year in anticipation of a pay hike. What they don’t realise is that pay hikes often lead to a higher cash outflow in the form of taxes. This can be avoided with a little planning and right communication to employers. If the payroll policy permits, one can explore the option of revising the compensation package to include tax-free components or modify the limits for each of the components as well as invest in tax deductible schemes.

Budgeting for a change

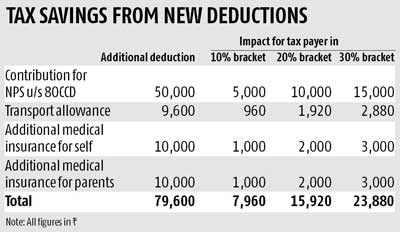

The Budget 2015-16 presents new avenues to save tax, which can be factored in while computing the monthly salary/tax deducted at source (TDS).

Transport Allowance: The limit has been enhanced for transport allowance from Rs 800 per month to Rs 1,600 per month. One needs to ensure that the enhanced limit is part of your compensation.

Section 80CCD: One can contribute to National Pension Scheme, or the NPS, to take advantage of an additional deduction of Rs 50,000 over and above the limit under section 80C. Those in the 30 per cent tax bracket will especially benefit, as they can save about Rs 15,000 in tax annually just by using the additional limit. Please note that 10 per cent of the salary contributed towards NPS is eligible for a tax deduction up to Rs 1.5 lakh under section 80CCD of the Act. Contributions by your employer are tax deductible in the NPS under Sec 80CCD(2). The total benefit under NPS can go up to Rs 2 lakh.

Section 80C: This section allows a maximum limit of Rs 1.5 lakh across investments such as provident fund, PPF, infrastructure bonds, five-year fixed deposits, Sukanya Samriddhi Account, NSC, insurance/pension plans, equity linked savings scheme. It also includes tuition fees of your children and the repayment of principal on your housing loan. Sukanya Samriddhi Account has been introduced this year and enables parents of a girl child less than 10 years old to claim deduction under the section. The scheme will earn 9.2 per cent for FY16 and is exempt-exempt-exempt, meaning the interest earned and the withdrawal amount will be exempt from tax.

Health care: Deduction under section 80D on health insurance prem

ium has been raised to Rs 25,000 from Rs 15,000 for individuals. For senior citizens, the limit has been raised to Rs 30,000 from the existing Rs 20,000. Deduction of Rs 30,000 is allowed toward medical expenditure for very senior citizen above the age of 80 years who are not eligible to take health insurance.

Charity: Donations made to certain institutions, are eligible for deduction subject to specified limits under section 80G. From this year, donations made to Clean Ganga Fund and Swachch Bharat Kosh will be eligible for 100 per cent deduction. There is no deduction available for donation made in excess of Rs 10,000 in cash.

Using existing options

House Rent Allowance (HRA): If the HRA is not part of your compensation structure yet, swapping a portion of other components with HRA could be a good tax saving option. The HRA component should especially be looked at by employees who have recently been transferred to new cities or shifted to rented accommodations. The salaried employees staying in rented apartments can claim exemption under Section 10(5) of the Income-Tax Act, 1961 (‘the Act’) in respect of house rent allowance by making the HRA a component of their salary. The Act provides for exemption for HRA subject to specified conditions and there could be a situation when the entire allowance is tax-free. If your annual rent exceeds Rs 1 lakh, you will need to submit a copy of your landlord’s PAN card to your employer.

Under section 80GG, an individual can claim deduction for the rent paid even if he does not get HRA, subject to certain conditions. The individual, his spouse or minor child should not own any house within the city limit or where he ordinarily resides or performs duties of his office, business or profession. The deduction will be the least of rent paid less 10 per cent of total income or Rs 2,000 a month or 25 per cent of total income.

Owned car versus leased car: In case an owned car is used partly for official purpose and partly for private purpose and where the employer reimburses expenses of Rs 10,000, the value of the perquisite is Rs 6,700 per month (for cars with engine capacities above 1.6 litres). In case a company leased car is used partly for official purpose and partly for private purpose and the expenses are reimbursed by the employer, the value of perquisite is Rs 3,300 per month. Most of the employers have a car scheme for their employees and if the vehicle is company-owned, this could result in significant tax savings for the employees though there would be some cash outflow towards the lease rentals, which is mostly a little less than the equated monthly instalment (EMI) for a car loan in case of an owned car.

Leave Travel Concession (LTC): Plan a holiday within India, take leave and save taxes, by claiming tax exemption on reimbursement of your travel expense. You can claim exemption for two journeys in a block of four calendar years. The amount is limited to the economy-class airfare for the shortest route available to your destination and does not include expenses such as hotel bills, local conveyance, etc. The current block of four years ends on December 31, 2017.